A “super-accelerated” drawdown of drilled, uncompleted wells could rapidly boost US oil production, with a new Rystad Energy analysis suggesting the Permian Basin alone could see an immediate 183,000 barrels per day (bpd) increase, alongside an additional 56,000 bpd from other regions.

Achieving this scenario would likely exceed theoretical limits, as it would require the Permian to utilise the entire currently available, idle frac fleet capacity, the Norway-based energy intelligence company said.

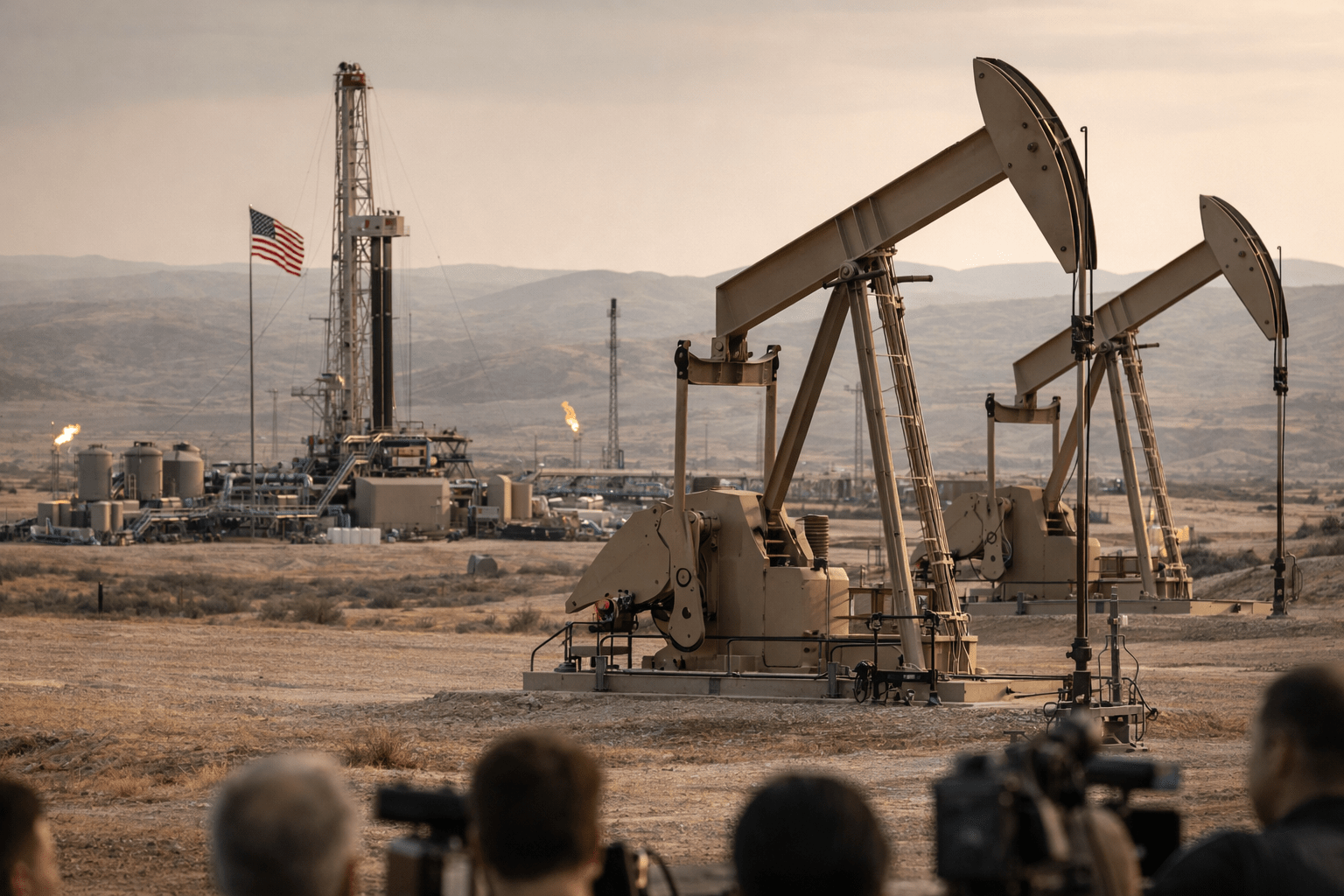

Despite the escalation of fighting between the US and Iran, which has caused oil prices to rise, US shale producers are still reluctant to increase their production.

“Even as US benchmark WTI prices sit above $90 per barrel, US shale producers are not poised to quickly ramp up production for two major reasons – strategic caution and a lack of DUCS to quickly bring online,” Matthew Bernstein, VP North America oil & gas at Rystad Energy, said in the analysis.

“Producers are currently using the opportunity to lock in higher revenues through hedging. Unless high prices last for months, shale E&Ps are unlikely to revise their plans, which budgeted for a challenging $55-60 WTI price.”

Capital discipline and 2025 DUC drawdown

US shale producers are maintaining capital discipline due to a cautious outlook on short-term price movements, driven by the steep backwardation of the WTI curve, which suggests the current price spike will be temporary.

Additionally, the availability of Drilled but Uncompleted wells is limited. This situation stems from low 2025 prices, which prompted producers to prioritise sustaining output and shareholder returns over capital expenditure (capex) spending, according to Rystad’s analysis.

“As a result, companies drew down excess DUC inventories and allocated cash to their balance sheet,” Rystad said.

“Even if producers are willing to grow, their ability to increase output quickly is hampered by last year’s DUC drawdown.”

Should the excess Drilled but Uncompleted wells in US shale be rapidly drawn down, this move could, within a few months, boost supply by an additional 111,000 barrels per day from these wells alone, the analysis showed.

A rapid drawdown is improbable because it would necessitate a coordinated strategic effort among numerous operators.

While some operators, likely private Exploration and Production (E&P) companies, will probably capitalise on the price surge by bringing Drilled but Uncompleted wells online, many public companies and supermajors will likely be cautious about further diminishing their productive capacity, the agency said.

Future production scenarios

Considering the conflict in the Middle East, the potential ways US production might react are as follow;

In a scenario where operators react to sustained high prices with a material increase in rigs over the next five months (46 total rigs added in Lower 48 oil plays), production would grow 196,000 bpd from exit 2025 rates to exit 2026, according to the analysis.

This is 280,000 bpd higher in December 2026 than Rystad’s pre-war base case.

The “maximum case” scenario assumes a significant production ramp-up across the Lower 48 states. While this reveals the theoretical short-term upside potential, it is currently considered extremely unlikely.

“We expect operators to apply a similar strategy to rig additions,” the agency said.

Disciplined cash rebuilding

Producers are currently choosing a disciplined strategy instead of immediately adding new rigs or drawing down their drilled but uncompleted wells.

Their first step is to add more hedges for the second quarter of 2026 through 2027, especially if they anticipate a price drop, and initial reports suggest active hedging by operators.

However, E&P companies structured their 2026 hedge books to provide protection against price decreases.

Since the peer group has only hedged about one-third of their production at low floor and ceiling prices, many might choose to simply benefit from the current spot market prices.

Private E&P companies that budgeted for prices near their break-even point might be the first to add an extra rig or frac crew.

This is because they can take advantage of expected second half of 2026 prices, which would still be higher than their original plan, even if they significantly drop from the $90-$100 range.

At the time of writing, the West Texas Intermediate crude oil was at $95.32 per barrel, down 0.2% from the previous close.

Compared to year-end 2024, pure shale E&Ps saw a decrease of over $4 billion in cash on their balance sheets by year-end 2025. This reduction resulted from E&Ps utilizing their cash reserves to sustain payouts to investors.

“With this in mind, producers will be in no rush to spend more capex in response to higher prices, and they will likely use the current period to rebuild cash on balance sheets at $100 oil while waiting to make any moves,” Rystad said.

The post Why US shale won't ramp up output fast even with WTI prices near $100/bbl appeared first on Invezz